Okay, I didn’t coin the phrase for this piece’s title—that was NY Yankee great Yogi Berra who came up with that line. Likewise, I didn’t come up with “it isn’t over until the fat lady sings” (Wagner opera), or “was it over when the German’s bombed Pearl Harbor?” (Bluto Blutarsky—Animal House). Regardless of one’s epitaph of choice, bond investors are slowly coming to the realization that historically—and by “historically” I mean every Fed rate hike cycle of the past 50-years—longer term bond yields tend to peak plus-or-minus a month around the LAST Fed rate hike of the cycle. And, in each of those previous rate hike cycles, the Fed wasn’t done until the targeted Fed Funds rate exceeded the peak inflation rate for that cycle, and almost always exceeded it by a lot.

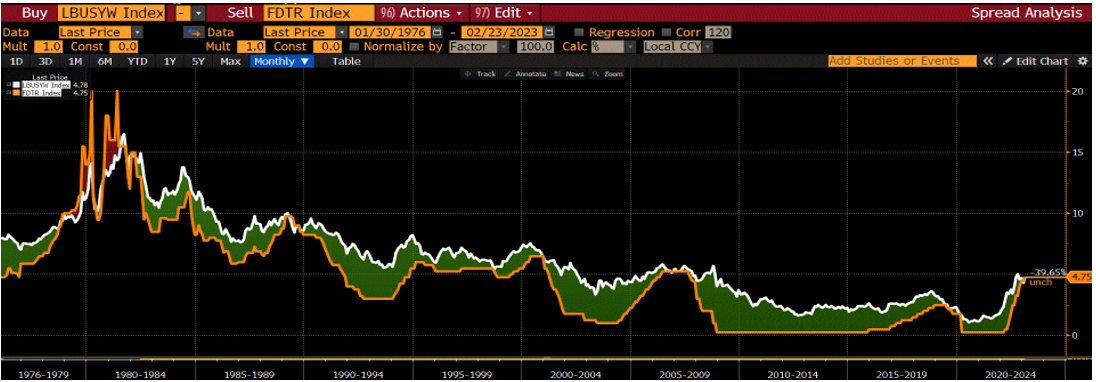

The chart below compares the yield for the target Fed Funds rate (orange line) to longer-term bond yields as measured by the Bloomberg Aggregate Bond Index (white line). As mentioned above, longer-term bond yields don’t typically peak until the Fed is at, or near, the end of its rate hikes.

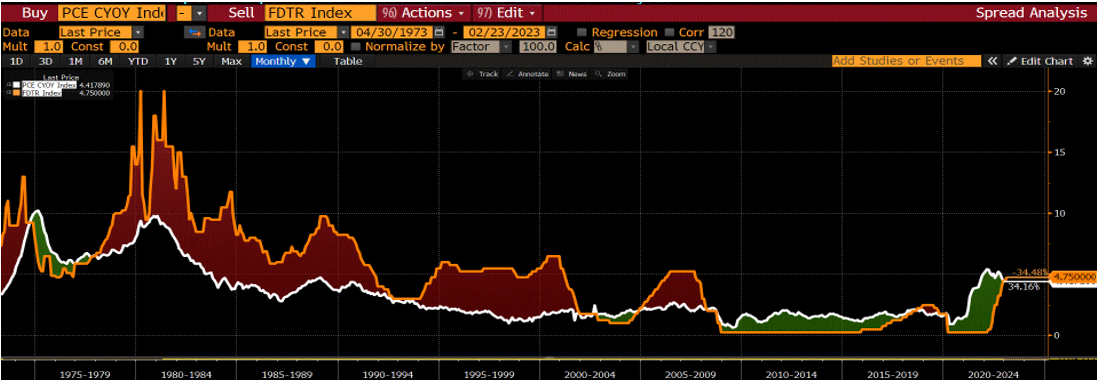

This next chart tells me the Fed may be a ways away from the end of this rate hike cycle. This chart compares the yield for the target Fed Funds rate (orange line) to the core inflation rate as measured by the Fed’s inflation index of choice the Core Personal Consumption Expenditure (PCE) Deflator. It is by far the most conservative inflation index. For the past 50 years Core CPI has been, on average, about 0.5% higher than the Core PCE Deflator, and is currently about 1.25% higher. As can be seen in the chart, every rate hike cycle since 1973 has ended with the target Fed Funds rate higher than the peak inflation rate of that cycle. The peak rate for the Core PCE Deflator, at least so far, was 5.4% (the peak for Core CPI was 6.6% and for total CPI it was 9.1%). That tells me that the Fed is almost certain to raise the target Fed Funds rate, at a minimum, to 5.5% (another 0.75% from current levels), and could go much higher.

Despite all of the Fed governors saying the exact same thing: we need to get rates higher and stay there for longer, the stock and bond markets have been anticipating a Fed pivot on the first sign of economic weakness. The markets’ reaction is understandable given the Fed, since Greenspan took over as Chairman in 1987, has been conditioning participants for the Fed “put”—i.e. the Fed will accommodate the markets at the first sign of trouble. The challenge with this cycle is that it doesn’t look like anything we’ve dealt with in the past 35 years. One needs to go back to the early-80s, pre-Greenspan, to find inflation levels similar to today. While Fed Chairman Arthur Burns didn’t figure it out, his successor Paul Volcker did—in order to snuff out spiraling inflation the Fed needs to raise rates higher than the inflation rate if it is going to be successful in breaking inflation. I believe the current Fed governors are well aware of Fed history.

The Fed rate hikes to date have only meaningfully slowed the most interest-rate sensitive part of the economy (housing). The unemployment rate is at its lowest peace-time level EVER, and wages continue to grow at twice the desired inflation rate of 2%. All of which says the Fed may feel it needs to go even higher with its rate hikes, and may have the room to do so given the strength of the services economy.

What’s a bond investor to do in such an environment? Until one is confident that longer-term yields have peaked; and, as noted above, we don’t believe that occurs until the Fed has signaled an end to this rate hike cycle, we believe alternative income strategies offer the best risk/reward value for investors. Our Robinson Alternative Yield Pre-Merger SPAC ETF (SPAX) could be part of that solution set. The pre-merger SPAC market continues to trade at an annualized discount to current trust value of about 3.5%; and, because the trusts are required by prospectus to invest in T-Bills or Treasury Money Market Funds, the trusts are growing at about a 4.5% annualized rate, which will increase one-for-one with any subsequent Fed rate hikes. The Bloomberg Aggregate Bond Index has a yield-to-worst of 4.78%, only slightly higher than T-Bill yields even though more than 12% of the index is invested in BBB-rated corporate bonds. In order to generate a 7.5% total return, the Bloomberg Aggregate Bond Index would need long-term yields to fall roughly 0.50%. It could happen. Of course, yields could also go up 0.50%, which would wipe out most of the 4.78% in income. Pre-merger SPAC investors avoid all that credit and interest rate risk, but don’t have to give up return in order to do so.

“It ain’t over till it’s over”, and the Fed has been telling the markets it may be some time before it’s over.

EXPLORE SPAX at www.robinsonetfs.com

ABOUT ROBINSON CAPITAL

Founded in December 2012, Robinson Capital Management, LLC, is an independent investment advisor specialized in developing traditional and alternative fixed income solutions. Robinson’s investment approach employs both fundamental and value techniques to best identify positive risk/reward opportunities and to maintain a consistent and disciplined approach. Robinson Capital also specializes in alternative value investing strategies, particularly through special purposes acquisition companies (SPACs) and closed-end mutual funds (taxable and tax-exempt).

Robinson Capital provides customized investment management services for RIAs, family offices, broker-dealers and institutions.

The firm serves as investment sub-adviser to the Robinson Alternative Yield Pre-Merger SPAC ETF (ticker: SPAX). For more information, visit, robinsonetfs.com.

DISCLOSURES

Investors should consider the investment objectives, risks, charges and expenses carefully before investing. For a prospectus or summary prospectus with this and other information about the Fund, click here. Read the prospectus or summary prospectus carefully before investing.

FUND RISKS

Investing involves risk. Principal loss is possible. ETFs may trade at a premium or discount to their net asset value. Brokerage commissions are charged on each trade which may reduce returns.

The Fund invests in equity securities and warrants of SPACs, which raise assets to seek potential business combination opportunities. Unless and until a business combination is completed, a SPAC generally invests its assets in U.S. government securities, money market securities, and cash. Because SPACs have no operating history or ongoing business other than seeking a business combination, the value of their securities is particularly dependent on the ability of the entity’s management to identify and complete a profitable business combination. There is no guarantee that the SPACs in which the Fund invests will complete a business combination or will be profitable.

Some SPACs may pursue a business combination only within certain industries or regions, which may increase the volatility of their prices. To the extent a SPAC or the fund is invested in cash or cash equivalents, this may impact the ability of the Fund to meet its investment objective. Investments in a SPAC may be considered illiquid and subject to restrictions on resale.

The Fund may purchase warrants to purchase equity securities. Investments in warrants are pure speculation in that they have no voting rights and pay no dividends. They do not represent ownership of the securities, but only the right to buy them. Warrants involve the risk that the Fund could lose the purchase value of the warrant if the warrant is not exercised or sold prior to its expiration. The Fund may also purchase securities of companies that are offered in an IPO. The risk exists that the market value of IPO shares will fluctuate considerably due to factors such as the absence of a prior public market, unseasoned trading, a small number of shares available for trading and limited information about the issuer. Such investments could have a magnified impact on the Fund.

Some sectors of the economy and individual issuers have experienced particularly large losses due to economic trends, adverse market movements and global health crises. This may adversely affect the value and liquidity of the Fund’s investments especially since the fund is non-diversified, meaning it may invest a greater percentage of its assets in the securities of a particular, industry or sector than if it was a diversified fund. As a result, a decline in the value of an investment could cause the Fund’s overall value to decline to a great degree.

The Fund is a recently organized management investment company with limited operating history and track record for prospective investors to base their investment decision.

The Fund is distributed by Foreside Fund Services, LLC.